by

by The global metal coil lamination market is projected to reach USD 8.71 billion by 2035, driven by increasing demand for lightweight, corrosion-resistant, and aesthetically advanced materials across construction, automotive, appliances, and industrial manufacturing sectors.

Introduction

The global metal coil lamination market is experiencing steady growth as industries increasingly demand durable, corrosion-resistant, lightweight, and visually appealing metal products. Metal coil lamination is widely used across construction, automotive, appliances, packaging, and industrial manufacturing applications to improve surface protection, aesthetics, thermal resistance, and product durability.

Rapid urbanization, infrastructure modernization, increasing electric vehicle production, and growing adoption of energy-efficient building materials are significantly accelerating market expansion worldwide. Manufacturers are also focusing on advanced coating technologies and sustainable production methods to meet evolving industrial and environmental standards.

Metal coil lamination involves bonding protective or decorative layers onto metal coils using various lamination techniques such as thermal lamination, adhesive lamination, and extrusion lamination. These laminated coils provide enhanced corrosion resistance, weather durability, insulation, and decorative finishes suitable for multiple end-use industries.

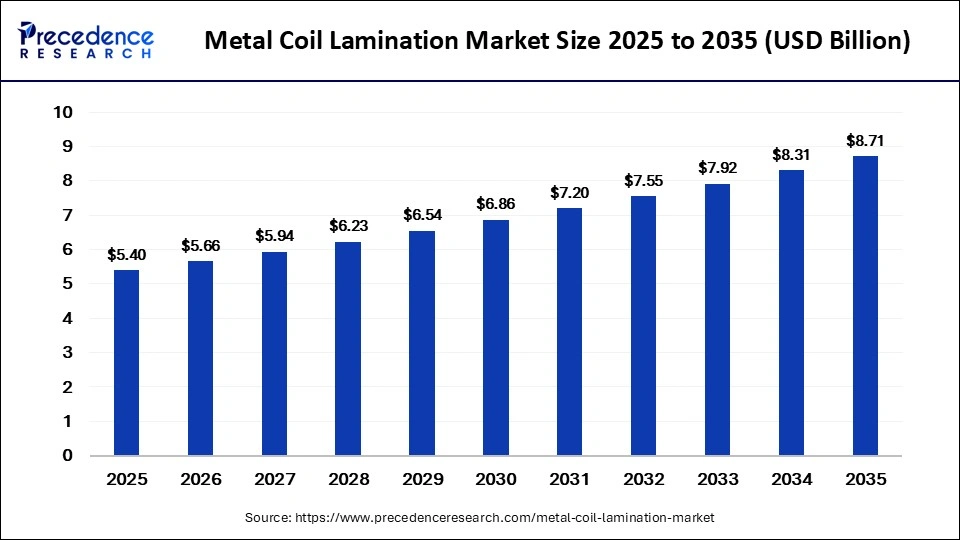

According to Precedence Research, the global metal coil lamination market size accounted for USD 5.40 billion in 2025 and is projected to increase from USD 5.66 billion in 2026 to approximately USD 8.71 billion by 2035, expanding at a CAGR of 4.90% during the forecast period.

Read Also: AI in Pharma Supply Chain Market

Metal Coil Lamination Market Overview

Metal coil lamination refers to the process of applying protective, decorative, or functional laminated coatings onto continuous metal coils such as steel, aluminum, stainless steel, and copper. These laminated materials enhance the durability, flexibility, thermal insulation, chemical resistance, and appearance of metal products used across industrial sectors.

The market is increasingly benefiting from the rising use of laminated metal products in smart appliances, energy-efficient buildings, automotive components, industrial machinery, and premium architectural applications. Manufacturers are focusing on advanced coating technologies capable of providing anti-corrosion, UV-resistant, moisture-resistant, and heat-resistant properties.

The increasing shift toward sustainable construction materials and lightweight transportation systems continues to create strong long-term opportunities for the industry.

Key Market Statistics

Major Market Highlights

- The metal coil lamination market is projected to grow at a CAGR of 4.90% from 2026 to 2035.

- Asia-Pacific accounted for 46% of global market share in 2025.

- Steel dominated the material segment with 52% market share in 2025.

- Thermal lamination led the market with 40% share in 2025.

- Polyester coating accounted for 34% market share in 2025.

- Building and construction applications represented 38% of market demand in 2025.

- Construction held 36% of end-use industry share in 2025.

- The 0.3–1 mm thickness segment accounted for 46% market share in 2025.

- Aluminum is projected to witness the fastest CAGR of 6.5% through 2035.

- Automotive applications are expected to grow at a CAGR of 6.2% during the forecast period.

Key Market Drivers

Rising Demand for Durable and Lightweight Materials

The increasing demand for durable, lightweight, and aesthetically attractive materials across industrial sectors is a major driver of market growth.

Industries such as automotive, construction, and appliances increasingly require laminated metal products that offer superior corrosion resistance, weather durability, thermal insulation, and visual appeal. Lightweight laminated materials help manufacturers improve operational efficiency while reducing overall material consumption.

The growing preference for energy-efficient and sustainable materials continues supporting demand for advanced metal coil lamination technologies.

Rapid Urbanization and Infrastructure Development

Rapid urbanization and large-scale infrastructure projects worldwide are significantly accelerating demand for laminated metal coils used in roofing, cladding, facades, industrial buildings, and commercial construction systems.

The building and construction segment accounted for 38% market share in 2025 because of rising global investments in residential, commercial, and industrial infrastructure.

Governments across emerging economies are increasingly promoting energy-efficient building materials and sustainable construction systems, further boosting market demand.

Expansion of Automotive Manufacturing

The automotive industry is becoming one of the fastest-growing application areas for metal coil lamination.

Automakers increasingly use laminated metal components to improve vehicle durability, corrosion resistance, and lightweight performance. The rapid growth of electric vehicles (EVs) is further accelerating demand for advanced coated and laminated materials.

The automotive segment is projected to expand at a CAGR of 6.2% during the forecast period due to rising global vehicle production and increased adoption of lightweight transportation materials.

Growing Demand for Smart Appliances and Consumer Electronics

The increasing production of smart appliances and consumer electronics is driving demand for visually appealing and durable laminated metal surfaces.

Manufacturers increasingly prefer laminated coils capable of providing premium finishes, moisture resistance, and improved surface aesthetics. Smart home appliance manufacturing growth continues supporting market expansion globally.

Impact of Artificial Intelligence on the Metal Coil Lamination Market

Artificial intelligence is increasingly transforming the metal coil lamination industry through smart manufacturing, automated inspection systems, and predictive maintenance technologies.

AI-powered visual inspection systems use machine learning algorithms and high-definition cameras to identify surface defects, coating inconsistencies, and production abnormalities with greater speed and accuracy. AI integration improves operational efficiency, product quality, and manufacturing consistency while reducing production costs and material waste.

Manufacturers are also leveraging AI for:

- Predictive maintenance

- Production optimization

- Smart coating management

- Quality assurance automation

- Energy consumption reduction

- Supply chain optimization

The growing adoption of Industry 4.0 technologies is expected to reshape the future of metal coil lamination manufacturing.

Market Trends

Increasing Demand for Customized and Premium Finishes

Manufacturers are increasingly focusing on innovative textures, premium finishes, and customized laminated coil designs for architectural and automotive applications.

Export markets particularly demand decorative laminated materials capable of mimicking wood, stone, marble, and premium metal surfaces. This trend is creating strong opportunities for advanced decorative coating technologies.

Expansion of Smart and Energy-Efficient Applications

The growing emphasis on energy-efficient appliances and smart electronics is increasing the adoption of laminated metal products capable of improving thermal management and modern aesthetics.

Smart appliance manufacturers increasingly rely on laminated metal systems to enhance product performance and design quality.

Growth of UV-Resistant and Anti-Corrosion Coatings

Advanced anti-corrosion, UV-resistant, and heat-resistant laminated coatings are emerging as major industry trends.

Industries increasingly require durable laminated layers capable of withstanding harsh environmental conditions while extending product lifespan.

PVDF coatings are gaining significant traction because of superior chemical resistance and UV protection capabilities.

Rising Focus on Sustainable Manufacturing

Sustainability is becoming a critical focus area across the metal coil lamination industry.

Manufacturers increasingly adopt water-based coatings, low-emission production systems, and recyclable laminated materials to comply with environmental regulations and carbon reduction goals.

The shift toward eco-friendly production technologies is expected to accelerate further over the next decade.

Market Restraints

Complex Coating and Application Challenges

Metal coil lamination involves highly complex manufacturing and coating processes.

Extreme temperatures, vibration exposure, and harsh operating conditions may create coating cracks or surface inconsistencies, affecting product durability and operational performance.

Maintaining consistent coating quality across large-scale manufacturing operations remains a significant industry challenge.

Volatility in Raw Material Prices

Fluctuating prices of steel, aluminum, copper, polymers, and coating materials continue affecting production costs and profit margins.

Global supply chain disruptions and geopolitical uncertainties may further impact pricing stability and raw material availability.

High Initial Investment Requirements

Advanced metal coil lamination systems require substantial capital investments in automated production lines, coating technologies, inspection systems, and quality control infrastructure.

Small and medium-sized manufacturers may face financial limitations when upgrading manufacturing capabilities.

Environmental and VOC Emission Regulations

Strict environmental regulations regarding volatile organic compound (VOC) emissions and industrial waste management continue creating compliance challenges for manufacturers.

Companies increasingly require investments in eco-friendly coating technologies and emission control systems to meet sustainability requirements.

Emerging Opportunities

Expansion of Electric Vehicle Manufacturing

The rapid global expansion of electric vehicle production is creating substantial opportunities for lightweight laminated metal materials.

Automotive manufacturers increasingly require advanced laminated coils capable of improving corrosion resistance, thermal efficiency, and lightweight vehicle design.

Rising Adoption of Aluminum Laminated Coils

The aluminum segment is expected to witness the fastest CAGR of 6.5% during the forecast period due to rising demand for recyclable, lightweight, and corrosion-resistant materials.

Aluminum laminated coils are increasingly used across automotive, construction, transportation, and appliances industries.

Increasing Demand for Sustainable Building Materials

Green construction initiatives and carbon-neutral infrastructure development are creating new opportunities for sustainable laminated metal systems.

Manufacturers adopting low-emission coating technologies and recyclable materials are expected to gain competitive advantages.

Growth in Emerging Economies

Rapid industrialization across Asia-Pacific, Latin America, and the Middle East is creating strong long-term demand for laminated metal products.

Infrastructure expansion, appliance manufacturing growth, and increasing automotive production continue supporting regional market development.

Segmental Analysis

By Material Type

Steel Segment Dominance

Steel dominated the market with 52% share in 2025 because of its extensive use across construction and industrial manufacturing applications.

Its high strength, affordability, and durability continue supporting strong market demand.

Aluminum Segment Growth

The aluminum segment accounted for 24% market share in 2025 and is projected to witness the fastest CAGR of 6.5% through 2035.

The growth is driven by increasing adoption of lightweight and recyclable materials in automotive and construction industries.

Stainless Steel and Copper Applications

Stainless steel and copper laminated coils continue witnessing steady growth because of increasing demand across healthcare, food processing, electronics, and industrial manufacturing sectors.

By Lamination Type

Thermal Lamination Leadership

Thermal lamination accounted for 40% market share in 2025 due to strong adhesion capabilities and cost-effective production processes.

Extrusion Lamination Growth

Extrusion lamination is projected to witness the fastest CAGR of 5.8% because of increasing demand for moisture-resistant and chemical-resistant coatings.

By Coating Type

Polyester Coating Dominance

Polyester coating held 34% market share in 2025 because of strong weather resistance and cost-effective construction applications.

PVDF Coating Expansion

PVDF coating is projected to grow at the fastest CAGR of 6% due to superior UV resistance and long-term durability.

By Application

Building and Construction Leadership

Building and construction applications dominated the market with 38% share in 2025 because of increasing infrastructure investments and urban development projects.

Automotive Application Growth

The automotive segment is projected to expand rapidly due to increasing EV production and rising demand for corrosion-resistant lightweight components.

Regional Analysis

Asia-Pacific

Asia-Pacific dominated the global metal coil lamination market with 46% share in 2025 and is projected to witness the fastest growth during the forecast period.

China, India, Japan, and South Korea remain major manufacturing hubs because of strong steel and aluminum production capacities, rapid infrastructure development, and growing automotive manufacturing activities.

China continues leading regional growth due to massive construction activities and increasing investments in advanced coated metal production technologies.

Europe

Europe accounted for 24% market share in 2025 and continues witnessing stable growth supported by strong automotive manufacturing and sustainable building initiatives.

The region increasingly focuses on lightweight materials, premium architectural applications, and energy-efficient construction technologies.

North America

North America continues witnessing steady demand driven by industrial modernization, commercial construction activities, and advanced appliance manufacturing.

The United States remains a major market for high-performance laminated metal products.

Middle East & Africa

The Middle East & Africa region is witnessing increasing demand because of infrastructure expansion, industrial development, and rising investments in construction and transportation sectors.

Key Companies in the Metal Coil Lamination Market

Major companies operating in the market include:

- Baowu Steel Group

- Ansteel Group

- Shougang Group

- ArcelorMittal

- Tata Steel

- Nippon Steel

- POSCO

- Thyssenkrupp

- JSW Steel

- JFE Steel Corporation

Get a Sample Copy: https://www.precedenceresearch.com/sample/8409

For inquiries regarding discounts, bulk purchases, or customization requests, please contact us at sales@precedenceresearch.com